What's in this article?

The mortgage industry is hemorrhaging money at an alarming rate. With an estimated $2 billion in annual excess costs directly attributed to poor lead quality, mortgage companies are facing their most expensive operational challenge in decades. Fannie Mae data reveals that income and employment errors now account for 50% of top loan defects, forcing expensive manual rework weeks into processing when these issues could have been caught upfront.

For mortgage professionals, this isn’t just about numbers on a spreadsheet anymore. It’s about survival in an increasingly competitive market where every dollar counts and every lead matters.

The Silent Productivity Killer

The statistics paint a sobering picture of what happens when lead quality deteriorates. While organic leads through SEO and content marketing can achieve conversion rates as high as 60%, the industry average for CRM-generated leads hovers around 20%. The gap between these numbers represents lost revenue, wasted resources, and frustrated mortgage loan officers (MLOs) who spend their time chasing prospects that were never qualified in the first place.

This productivity drain extends far beyond individual transactions. MLOs overwhelmed by junk leads spend disproportionate amounts of time filtering out bad prospects, eroding trust, morale, and their ability to close viable deals. The result? A retention crisis that’s costing companies their top talent just when they need it most.

The Real Cost of Cheap Leads

The temptation to chase low-cost leads is understandable, especially when marketing budgets are tight. However, the true cost calculation reveals a different story entirely. Shared leads sold to multiple lenders have markedly lower conversion rates and higher dropout rates compared to exclusive, high-quality leads.

| Lead Type | Average Conversion Rate | Cost per Acquisition | Total Cost per Close |

| Organic/SEO | 60% | $50 | $83 |

| Exclusive Verified | 45% | $150 | $333 |

| Shared/Bulk | 20% | $25 | $125 |

| Trigger Leads | 15% | $15 | $100 |

The table above demonstrates why focusing solely on lead cost per acquisition is a dangerous mistake. When you factor in conversion rates, the cheapest leads often become the most expensive closes.

The AI Revolution in Lead Management

Forward-thinking mortgage companies are leveraging artificial intelligence to address the lead quality crisis head-on. AI-powered solutions are transforming how lenders approach lead scoring, verification, and management through several key innovations:

Automated Underwriting and Scoring

Machine learning models trained on historical conversion, default, and defect data can rank and route leads by predicted value and risk before they reach human hands.

Shift-Left Verification

Integrating automated income and employment verification earlier in the application journey catches and resolves issues before resource-intensive underwriting stages begin.

Predictive Analytics

Advanced algorithms identify likely converters and flag potentially problematic leads earlier in the pipeline, allowing MLOs to focus their energy on prospects with genuine potential.

The impact is measurable. Companies implementing these AI-driven approaches report significant improvements in processing times, borrower satisfaction, and most importantly, bottom-line results.

Five Strategies to Eliminate Junk Leads Forever

1. Implement Multi-Tiered Screening

Use layered data enrichment and validation to weed out duplicate, incomplete, or fraudulent leads prior to MLO assignment. This approach creates multiple checkpoints that catch problematic prospects before they consume valuable resources.

2. Source Strategically

Work only with carefully screened lead providers and favor exclusive leads over shared ones. Regular vendor audits ensure your lead sources maintain quality standards over time.

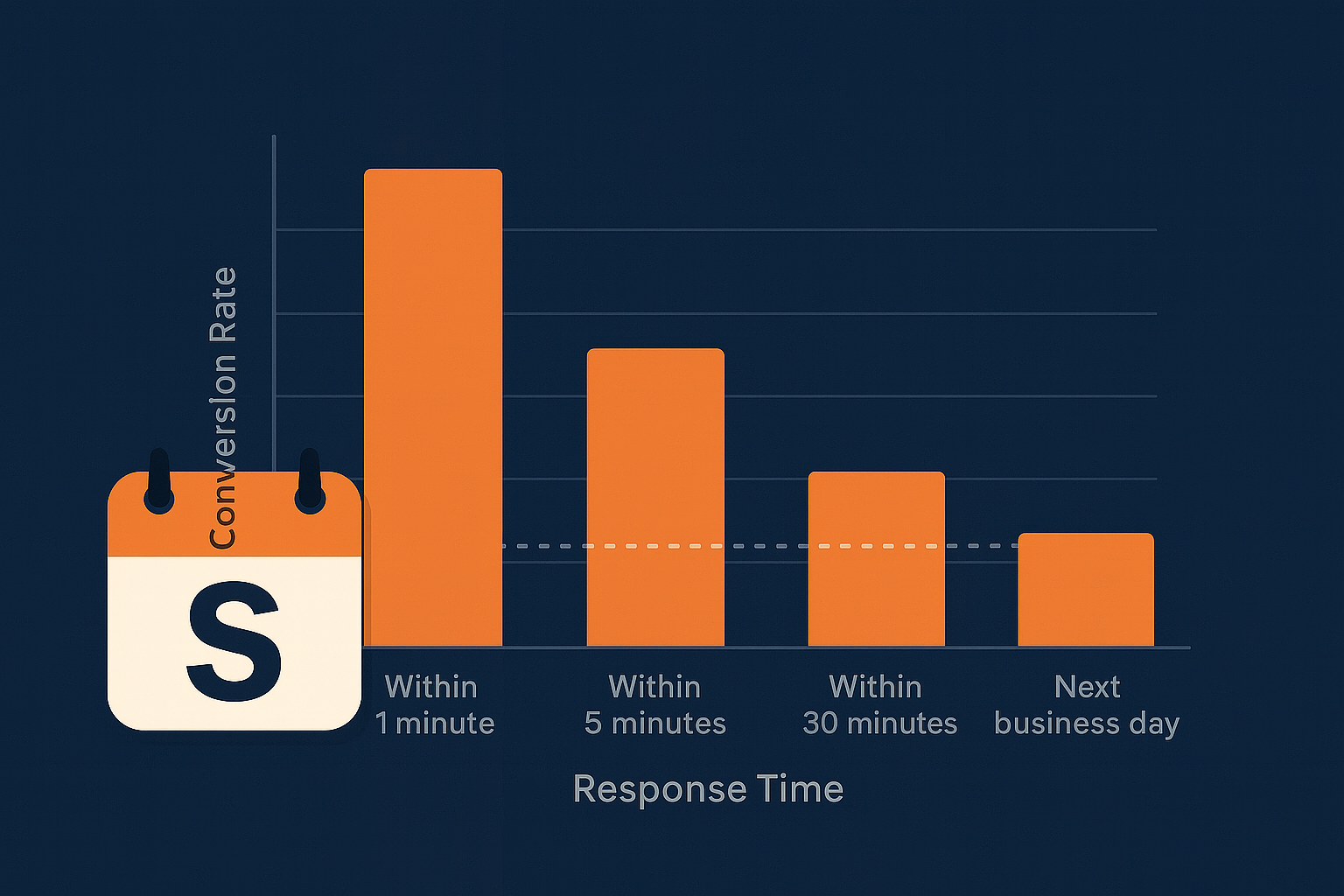

3. Optimize Response Time

High-quality leads are often contacted by multiple parties due to practices like trigger leads. Companies that respond fastest capture the highest conversion rates and build stronger borrower relationships from the first interaction.

4. Deploy Real-Time Verification

Validate contact details, employment status, and financial capacity instantly using API-driven verification tools. This eliminates the weeks-long discovery of basic disqualifiers that plague traditional processes.

5. Create Quality Feedback Loops

Establish regular analysis of lost leads and loan defects to continuously refine acquisition strategies. What you learn from failures becomes the foundation for future success.

The Competitive Advantage of Quality

As the industry projects a 30% increase in non-QM lending in 2025, the strain on verification systems already at capacity will deepen. Companies that invest now in upstream AI and stricter lead verification practices will find themselves with a significant competitive advantage over those still relying on outdated manual processes.

The mathematics are simple: higher-quality leads result in better margins, lower fallout rates, and more satisfied MLOs who can focus on what they do best—closing loans and building relationships with qualified borrowers.

Frequently Asked Questions

Q: What’s considered a good conversion rate for mortgage leads in 2025?

A: Conversion rates vary significantly by lead source. Organic leads can achieve 60% conversion, while exclusive verified leads typically convert at 45%. Industry averages for most lead sources hover around 20–25%.

Q: How much do poor-quality leads actually cost mortgage companies?

A: The industry faces an estimated $2 billion in annual excess costs due to poor lead quality, with income and employment errors accounting for 50% of loan defects that require expensive late-stage corrections.

Q: Can AI really improve mortgage lead quality?

A: Yes, AI-powered lead scoring and verification tools can identify likely converters and flag problematic leads before they consume resources. Companies using these tools report significant improvements in processing efficiency and conversion rates.

Q: Should I avoid shared leads entirely?

A: Shared leads consistently show lower conversion rates and higher dropout rates compared to exclusive leads. While they may appear cheaper upfront, the total cost per closed loan is often higher due to poor conversion performance.

Transform Your Lead Strategy Today

The mortgage lead quality crisis isn’t getting better on its own. Every day you delay implementing a comprehensive lead management strategy, your competitors are gaining ground while your costs continue to climb. The companies that will thrive in 2025 and beyond are those taking action now to transform their approach to lead acquisition, verification, and management.

ProPair.ai’s AI-powered lead management platform helps mortgage companies eliminate junk leads, optimize conversion rates, and empower their MLOs with only the highest-quality prospects. Stop wasting money on leads that will never close and start building a sustainable competitive advantage.