What's in this article?

The Silent Profit Killer Hiding in Your Operations

Every day, mortgage companies across America unknowingly hemorrhage profits through an outdated practice that seems harmless on the surface: manual lead qualification. While executives focus on lead generation costs and conversion rates, a more insidious problem drains resources behind the scenes.

The shocking reality? Mid-sized mortgage lenders lose over $1 million annually through manual lead qualification inefficiencies. This isn’t hyperbole—it’s math based on current industry data that most companies haven’t calculated.

With mortgage origination costs hitting $11,600 per loan in 2024 and labor representing the largest expense category, the cost of maintaining manual processes has reached a breaking point. The question isn’t whether your company can afford to automate—it’s whether you can afford not to.

Breaking Down the Million-Dollar Loss

Lead Acquisition Costs Are Just the Beginning

The mortgage lead landscape in 2024 presents a stark financial reality:

| Lead Type | Exclusive Cost | Shared Cost |

| Purchase Mortgages | $40–$100+ | $15–$40 |

| Refinance Leads | $35–$85 | $12–$35 |

| Reverse Mortgages | $55–$150 | $25–$70 |

| FHA/VA/Jumbo | $50–$120 | $20–$50 |

But here’s where most companies miscalculate: lead cost is only the entry fee. The real expense comes from what happens next.

The Hidden Labor Drain

Manual lead qualification demands significant human resources for document review, verification calls, and prospect communication. Current industry data reveals that manual processes require 2.2–4.7 additional staff hours per loan compared to automated systems.

With fulfillment costs averaging $3,483 per loan for retail channels and $4,077 for consumer-direct, the labor component represents the majority of origination expenses. When you factor in the extended time manual qualification requires, each loan processed manually costs $400–$1,000 more in labor alone.

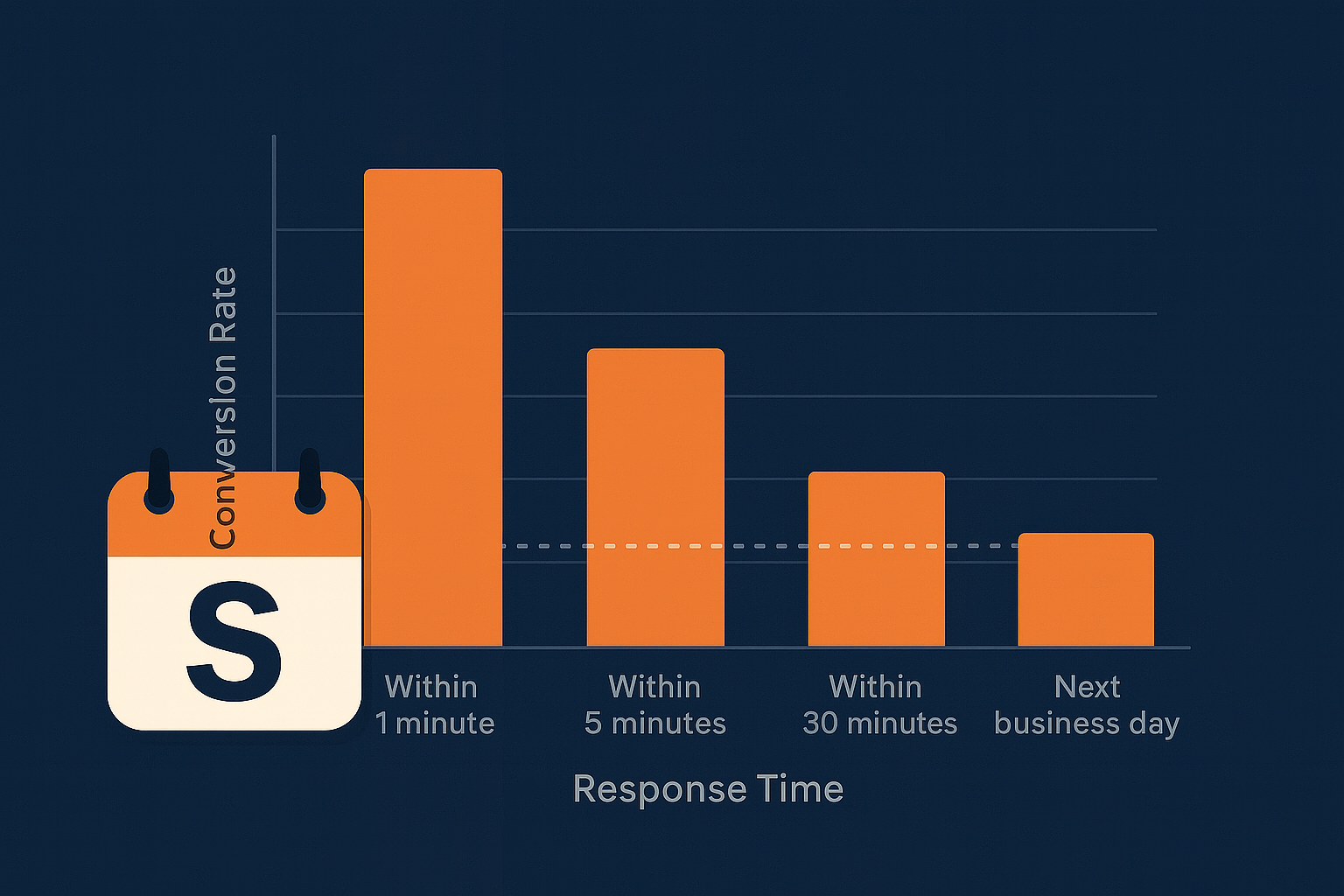

Conversion Rate Reality Check

The performance gap between manual and automated lead qualification is substantial:

- Automated systems: Conversion rates up to 60% for high-quality leads

- Manual CRM management: Approximately 20% conversion rates

- Time to first contact: Automated systems respond instantly; manual processes often delay by hours or days

This delay is costly. Industry research consistently shows that lead conversion rates drop dramatically with each passing hour after initial inquiry.

The Compound Effect of Inefficiency

Volume-Based Cost Multiplication

Consider a mid-sized lender processing 1,000 loans annually:

- Extra labor per loan: 3.5 hours (average)

- Blended hourly cost: $65 (including benefits and overhead)

- Additional labor cost per loan: $227.50

- Annual excess labor cost: $227,500

But this calculation only covers direct labor. Add in:

- Lower conversion rates from delayed response

- Compliance risks from manual errors

- Opportunity costs of skilled staff performing routine tasks

- Technology redundancies maintaining multiple systems

The total easily exceeds $1 million for companies processing moderate volume.

The Scaling Problem

As loan volume increases, manual processes create exponential inefficiency. Companies often respond by hiring more staff, which temporarily masks the problem while amplifying long-term costs. This creates a cycle where growth actually reduces profitability per loan.

Real-World Impact on Business Operations

Staff Utilization Issues

Manual lead qualification traps experienced mortgage professionals in repetitive tasks. Skilled loan officers and processors spend hours on data entry and verification work that automation handles instantly. This misallocation prevents teams from focusing on relationship building, complex problem-solving, and revenue-generating activities.

Customer Experience Degradation

Delayed response times hurt more than conversion rates—they damage brand reputation. In today’s instant-communication environment, prospects expect immediate acknowledgment and quick follow-up. Manual processes simply cannot compete with borrower expectations.

Competitive Disadvantage

While your company manually reviews leads, competitors using automated qualification systems are already engaging prospects, scheduling appointments, and moving toward application completion. This speed differential compounds over time, creating significant market share implications.

Quantifying Your Company’s Specific Loss

To calculate your manual qualification costs, examine these key metrics:

Direct Labor Analysis:

- Average time spent per lead during initial qualification

- Hourly cost of staff performing qualification tasks

- Volume of leads processed monthly

- Current conversion rates from lead to application

Indirect Cost Factors:

- Lead follow-up cycles and abandonment rates

- Compliance errors requiring rework

- Technology costs for multiple manual systems

- Training time for new qualification staff

Most companies discover their actual costs exceed initial estimates by 40–60% once all factors are considered.

Frequently Asked Questions

How much does manual lead qualification actually cost compared to automation?

Manual lead qualification typically costs $400–$1,000 more per loan than automated systems, factoring in extended labor hours, lower conversion rates, and compliance risks. Automation eliminates 2.2–4.7 staff hours per loan on average.

What’s the typical ROI timeline for mortgage lead qualification automation?

Most companies see ROI within 6–12 months, with reported returns ranging from 100–300%. The payback period depends on current volume and the degree of manual processes being replaced.

Can smaller mortgage companies justify automation costs?

Companies processing as few as 200 loans annually often justify automation investments. The key is calculating total cost of manual processes, including opportunity costs and competitive disadvantages.

What happens to staff when lead qualification becomes automated?

Successful companies redeploy staff to higher-value activities like relationship management, complex underwriting, and business development rather than reducing headcount.

Transform Your Lead Qualification Process Today

The mortgage industry has reached a tipping point where manual lead qualification represents a competitive liability rather than a cost-saving measure. Companies continuing these practices face mounting disadvantages that compound monthly.

Start with a comprehensive audit of your current lead handling process. Track actual time spent, measure true conversion rates, and calculate total labor costs including overhead. Most companies discover their manual processes cost significantly more than automation alternatives.

The mathematics are clear: automation isn’t just about efficiency—it’s about survival in an increasingly competitive market where speed and accuracy determine success.